VA Home Loans: Your Course to Absolutely No Down Payment Home Financing

VA Home Loans: Your Course to Absolutely No Down Payment Home Financing

Blog Article

The Necessary Guide to Home Loans: Unlocking the Benefits of Flexible Funding Options for Your Dream Home

Navigating the intricacies of home lendings can commonly really feel difficult, yet recognizing flexible financing choices is crucial for potential property owners. With a range of loan types offered, consisting of government-backed options and adjustable-rate home loans, debtors can customize their funding to straighten with their individual financial scenarios. These versatile alternatives not just provide lower initial payments however might likewise use one-of-a-kind advantages that boost accessibility to homeownership. As you think about the myriad of options, one must ask: what aspects should be focused on to make certain the most effective suitable for your financial future?

Recognizing Home Loans

Comprehending mortgage is important for prospective home owners, as they represent a significant economic commitment that can influence one's monetary health for several years to find. A home funding, or mortgage, is a kind of financial obligation that permits individuals to obtain money to acquire a property, with the residential or commercial property itself offering as collateral. The lending institution offers the funds, and the borrower accepts settle the funding amount, plus rate of interest, over a specific period.

Trick components of home loans include the major amount, rate of interest, loan term, and regular monthly settlements. The principal is the original finance amount, while the passion rate figures out the price of borrowing. Financing terms normally range from 15 to thirty years, affecting both monthly settlements and overall interest paid.

Sorts Of Flexible Funding

Adaptable funding options play a vital function in accommodating the varied requirements of homebuyers, allowing them to tailor their home mortgage options to fit their financial scenarios. One of one of the most common kinds of versatile funding is the adjustable-rate home loan (ARM), which provides a first fixed-rate period followed by variable prices that change based on market conditions. This can provide reduced initial settlements, attracting those that expect revenue growth or strategy to move prior to rates change.

Another choice is the interest-only home loan, allowing borrowers to pay only the interest for a specific duration. This can cause reduced regular monthly payments originally, making homeownership more available, although it may result in bigger payments later.

Furthermore, there are additionally hybrid finances, which incorporate features of taken care of and variable-rate mortgages, providing stability for a set term complied with by modifications.

Last but not least, government-backed lendings, such as FHA and VA fundings, use adaptable terms and reduced down payment requirements, accommodating novice purchasers and professionals. Each of these choices provides one-of-a-kind advantages, permitting homebuyers to select a financing solution that aligns with their long-term financial goals and personal scenarios.

Advantages of Adjustable-Rate Mortgages

How can variable-rate mortgages (ARMs) benefit property buyers looking for affordable financing alternatives? ARMs provide the capacity for lower preliminary rates of interest compared to fixed-rate home mortgages, making them an attractive option for customers looking to decrease their regular monthly settlements in the early years of homeownership. This initial period of lower prices can considerably improve price, permitting property buyers to invest the financial savings in various other priorities, such as home improvements or cost savings.

In addition, ARMs typically come with a cap framework that restricts exactly how much the passion rate can enhance during modification periods, supplying a level of predictability and protection against severe variations in the market. This attribute can be specifically advantageous in a rising interest price setting.

Furthermore, ARMs are ideal for customers that prepare to offer or refinance before the car loan adjusts, allowing them to take advantage of the reduced rates without direct exposure to prospective rate increases. Because of this, ARMs can work as a calculated financial device for those that fit with a degree of threat and are seeking to maximize their acquiring power in the existing housing market. Generally, ARMs can be a compelling choice for wise property buyers seeking versatile financing remedies.

Government-Backed Finance Choices

FHA loans, guaranteed by the Federal Housing Administration, are ideal for first-time property buyers and those with reduced credit report. They usually need a reduced deposit, making them a prominent selection for those who may have More Help a hard time to conserve a substantial amount for a standard lending.

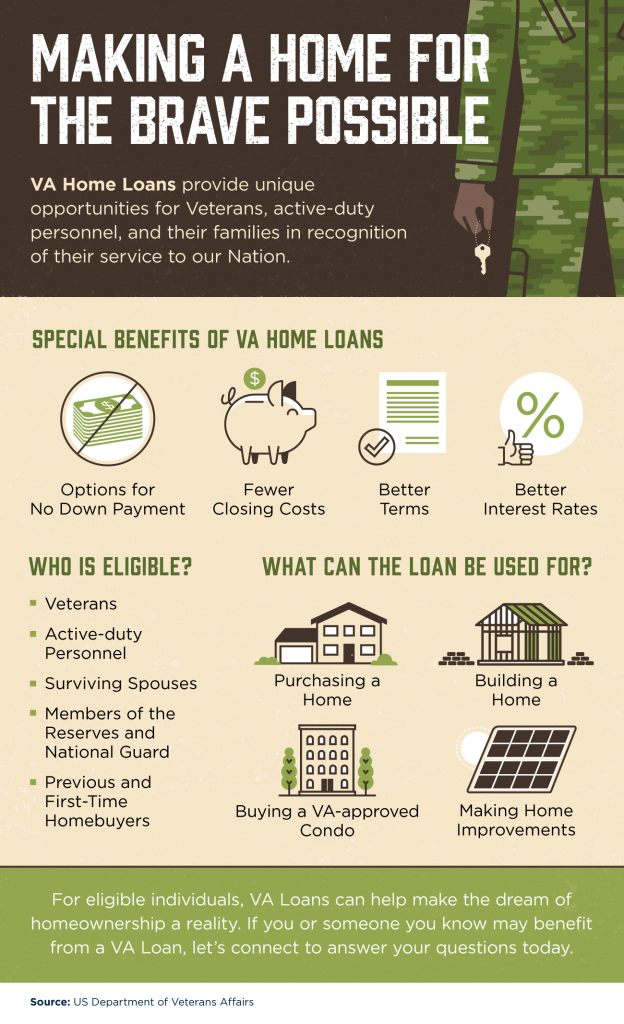

VA lendings, offered to professionals and active-duty armed forces workers, provide beneficial terms, including no deposit and no personal mortgage insurance (PMI) This makes them an eye-catching alternative for qualified debtors seeking to acquire a home without the burden of additional costs.

Tips for Choosing the Right Loan

When examining loan choices, consumers typically take advantage of thoroughly examining their economic situation and long-lasting objectives. Beginning by determining your budget plan, which consists of not just the home purchase cost however additionally additional expenses such as property taxes, insurance coverage, and upkeep (VA Home Loans). This comprehensive understanding will assist you in picking a funding that fits your economic landscape

Next, think about the sorts of lendings offered. Fixed-rate mortgages provide security in regular monthly settlements, while variable-rate mortgages might provide lower initial prices but can fluctuate over time. Assess your risk tolerance and how much time you plan to remain in the home, as these elements will influence your lending choice.

Additionally, scrutinize interest try this website prices and fees associated with each car loan. A lower rates of interest can dramatically reduce the total cost over time, yet be conscious of closing expenses and other costs that may balance out these cost savings.

Conclusion

In final thought, navigating the landscape of home lendings discloses various versatile financing choices that provide to diverse debtor demands. Comprehending the intricacies of different funding kinds, including government-backed fundings and adjustable-rate home mortgages, enables notified decision-making.

Browsing the intricacies of home loans can typically really feel challenging, yet comprehending adaptable funding alternatives is important for prospective house owners. A home loan, or mortgage, is a type of financial debt that permits people to obtain money to purchase a building, with the residential property itself offering as security.Trick parts of home lendings consist of the major amount, interest rate, finance term, and month-to-month settlements.In conclusion, navigating the landscape of home fundings reveals many adaptable financing choices that provide to varied consumer demands. Comprehending the complexities of different car loan types, including adjustable-rate mortgages and government-backed loans, makes it possible for educated decision-making.

Report this page